Buy-now-pay-later (BNPL) companies help to take the sting out of a purchase by allowing customers to make payments, usually paying in 4 installments.

Unlike credit cards and personal loans, this is a type of short-term financing that doesn’t typically come with interest or extra fees.

BNPL companies pay the retailer in full on your behalf today in exchange for your agreement to make a series of smaller payments.

Here are some reasons why you might use a buy-now-pay-later website or app:

- You don’t have a credit card.

- You’re purchasing from a retailer or company that doesn’t offer financing options.

- Your poor credit history makes it hard to obtain traditional financing.

- You don’t have the funds to cover a purchase.

- You are trying to stick to a monthly budget.

BNPL financing is obtained at checkout with online and in-person retailers. Once approved, a shopper usually provides a down payment totalling anywhere from 10% to 30% of the purchase.

The rest will be paid off in installments over the course of several weeks or months.

Most BNPL companies require the customer to set up autopay using a debit card, credit card, or bank account.

The fact that buy-now-pay-later platforms don’t charge interest or fees may have you scratching your head as you wonder how these companies make money.

They actually earn money by taking a cut of each sale the retailer makes. As a point-of-sale service, BNPL helps retailers because it helps more people to purchase products even if they can’t pay the full amount today.

BNPL has exploded in recent years! Which buy-now-pay-later platform is the best? It depends on the features a purchaser wants.

Take a look at 10 popular buy-now-pay-later sites and apps that allow to pay in 4 installments or more.

Please note that the listing below is in no particular order.

Of course, it’s important to always read the terms of any financing platform before signing up to make a purchase!

1. Klarna

Almost everyone who shops online has seen the Klarna icon near the checkout box by now.

This is one of the most popular BNPL apps for clothing retailers today. Klarna splits all purchases into four equal payments spread out over six weeks.

After collecting the first payment at checkout, Klarna then collects the remaining three payments every two weeks.

In addition to providing financing, Klarna also offers a shopping portal where you can find deals on the items you were already going to buy.

The Klanra app also tracks and updates shipping for all your online orders in one spot. You can even use Klarna to purchase in-store items using flexible payments.

2. Zip

Zip lets customers split nearly any purchase into four installments paid over six weeks.

The twist here is that Zip is accepted nearly everywhere Visa is accepted. That means it can be used to shop online, pay bills, book vacations, order groceries, and make in-store purchases.

While Zip doesn’t charge interest, there’s a $7.95 monthly account fee.

3. Afterpay

Afterpay lets shoppers break purchases up into four interest-free installment payments over six weeks.

Afterpay also allows shoppers to make in-store purchases by syncing the app with Apple Wallet or Google Wallet. After creating an Afterpay account, shoppers can begin earning rewards every time they shop with select retailers.

4. Affirm

Affirm allows shoppers to extend the repayment period for up to a year by paying interest.

Under the standard option, Affirm shoppers make four payments over eight weeks. Any possible interest will be shown beforehand so you know how much interest you will pay over time.

Customers can extend the repayment period to six months or 12 months by agreeing to pay %10.00 Annual Percentage Rate (APR). Affirm works for both online and in-store purchases.

5. PayPal Pay in 4

While PayPal has been around as a quick-pay platform since 1998, the company has evolved to offer buy-now-pay-later services.

For purchases between $30 and $1,500, customers can make four interest-free bi-weekly payments.

When making purchases between $199 and $10,000, customers can choose to make six, 12, or 24 monthly payments with 9.99% to 29.99% APR. PayPal Purchase Protection is available for free on eligible purchases.

6. Sezzle

While most BNPL platforms don’t have any effect on the shopper’s credit score, Sezzle actually markets itself as a credit-building tool!

The company claims that the average user sees their credit score jump by 20 points within four months of signing up.

Like standard BNPL platforms, Sezzle lets shoppers pay for purchases using four interest-free installments over six weeks. When customers use the app to simply pay in full, they can earn up to 2% in Sezzle Spend credits.

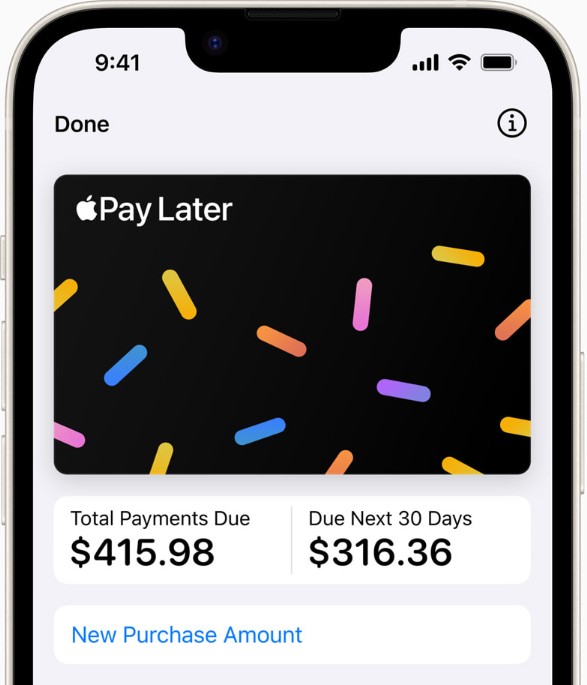

7. Apple Pay Later

Apple Pay Later is one of the giants in BNPL. In partnership with the Mastercard Installments program, Apple allows shoppers to make four interest-free payments over six weeks.

Additionally, users can apply for financing through Apple Pay Later Loans totaling between $50 and $1,000. These loans are designed specifically to make it easier to purchase an iPhone or iPad with a merchant that accepts Apple Pay.

8. Four

Four is a BNPL platform that’s slowly rising in popularity. It follows the standard model of allowing shoppers to split payments into four interest-free payments.

The perk of Four is that it syncs easily with Apple Pay and Google Pay to make online shopping breezier for those who don’t want to use their credit or debit cards.

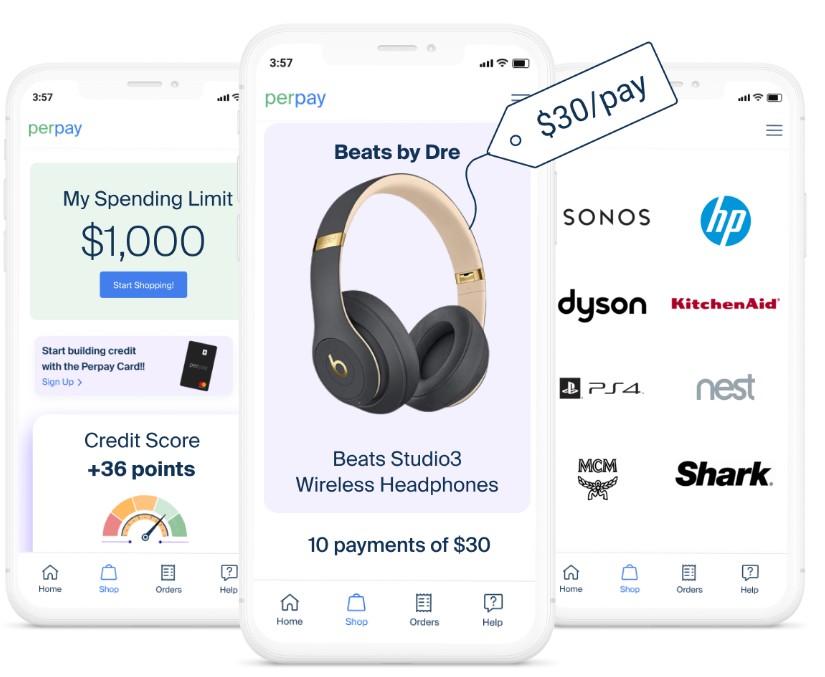

9. Perpay – Shop and Build Credit

Perpay is geared toward shoppers who want to use their purchases to build good credit.

The big differentiator here is that users automatically pay for their orders over time using direct deposit from each paycheck they earn.

While Perpay works with many major retailers, it can’t be used everywhere. It also has some stringent requirements.

A new user must have a full-time job, proof of three months of income, be free of active bankruptcies, and own a mobile phone.

10. Splitit

Splitit is a payment option that allows shoppers to increase their buying power while getting all of the perks and benefits of paying with their ordinary credit cards.

Look at it like a pre-authorization service that allows you to pay your credit card bill on time every month to avoid accruing interest.

Once you choose the number of payments you want to make, Splitit authorizes the full amount of the total to reserve your balance until you’ve made your final payment.

Splitit charges your credit card the installment amount without extra fees or interest every month until the payment plan is finished.

Leave a Reply