In these unprecedented times, our monetary minds are racing with negative thoughts, feelings, and bucketloads of stress.

It’s about time you were given some financial freedom, right? These apps (and the companies behind them) aim to do just that.

The main one being Dave, of course. You’ve probably heard of it. But if you haven’t don’t worry, we’re going to tell you all about it.

And then, we’re going to show you 12 other smartphone apps you can use that are similar if Dave doesn’t take the cake for you.

Are you ready? Let’s get into the details.

What Is the Dave App?

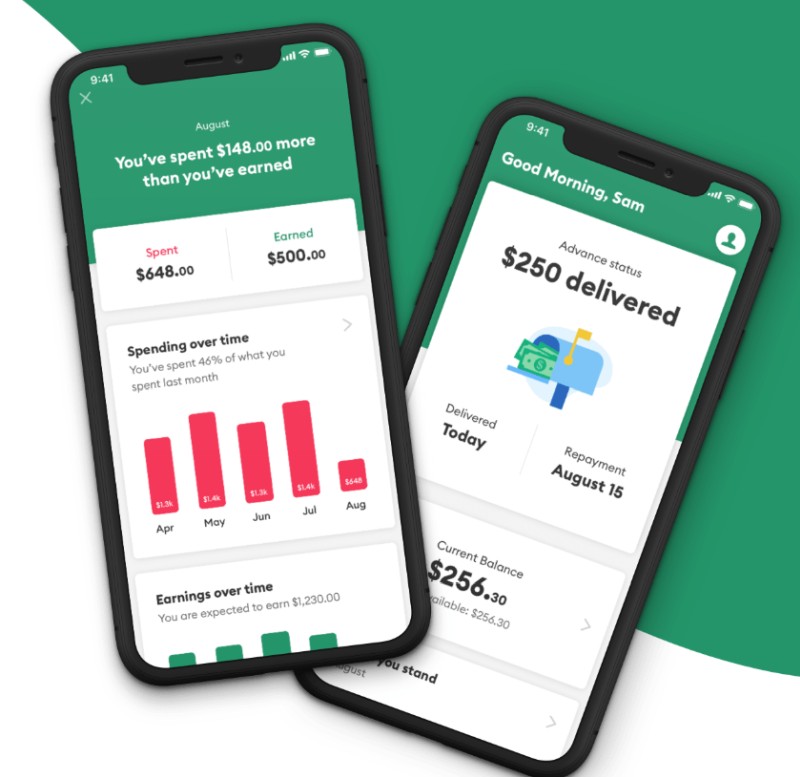

Dave is an app that offers its members cash advances. Why? So you can stave off those awful overdraft fees!

The greatest thing about it is that the app does not charge interest. Instead, it asks for tips (which, by the way, are completely optional).

It’s also handy since it sends you a notification when your checking account is low and will ask if you need a cash advance to tide you over. As you can imagine, this has saved a lot of people!

Although, it should be noted that you will have to pay a monthly fee which is just $1 per month. Plus, the max amount of cash advance you can get is relatively low.

The Pros

- No interest charged but you can give tips (optional)

- Lets you know when your bank account looks like it’s going to tip into overdraft

- Gives you budgeting tools

- Suggests “side hustles” for you to make a bit of extra cash every month

The Cons

- Maximum cash advance is low

- Membership fee of $1 per month

- Takes money out of your bank account automatically for repayments

Although Dave cash advance app is great, some people look for more options. Fortunately there are many similar financial apps that can help you during “rainy days”.

(The ranking below is in no particular order).

1. Brigit

Just like Dave, Brigit allows you to ask for a cash advance if you’re about to hit your overdraft. It’s incredibly easy to connect it to your current account, and from there, it will investigate your expenses and let you know when you’re running low.

When it realises you are going to be overdrafted, it offers a personalised suggestion that will cover you until you get your paycheck.

Plus, you can set up automatic advances if you’re super busy and don’t have time to approve every suggestion.

The Pros

- Repayment dates can be extended

- Analyses your spending habits

- Personalised cash advance suggestions

- Can set up automatic advances

- No interest

- No late fees

The Cons

- Customer support is only via email

- Monthly fee of $9.99

- No joint bank accounts allowed

2. Possible Finance

This one is a little different. It is an app that provides short-term installment loans. The maximum amount you can borrow is $500, which, so far, is the biggest loan amount we’ve seen here today! Typically, it will cost you around $30 for every $200 you borrow (with 8-weeks repayment).

Possible Finance operates a term lasting two months. To repay your installment loan you’ll deposit 4 payments across 8 weeks until you’ve paid everything.

If this seems scary right now, it’s a great thing! Once you’ve completed the repayments, the app will report this to the credit bureaus. So, you can rack up a great score over time.

The Pros

- Repayment terms align with your payday

- No credit check

- Rebuild your credit score

- Great customer service

The Cons

- Some technical issues

- Not an advance app

- Limited availability

3. Earnin

Earnin aims to be the place where you can go to find financial fairness. They claim to solve the following:

- Unfair overdraft fees

- Extortionate medical bills

- Finding ways to get extra cash

- Paydays hold back money for a long time

The app offers small advances to tide you over until you get your next paycheck. You won’t be liable to pay overdraft fees, payday loans or credit card fees this way.

Oh, and you get all this without paying for a membership fee!

The Pros

- Community driven

- No membership fees

- No credit score check needed

- Lots of other tools to access

- Plenty of budgeting resources

The Cons

- Low advance limits

- The tips can get expensive

- You’d be sacrificing a certain degree of privacy

- Only certain workers can access it

4. Branch

Branch is an app that lets you ask for an advance on your paycheck. It makes use of a platform called Pay which is far cheaper than the average payday loan.

You won’t need to pay the high-interest rates that are associated with loan sharks. Instead, you can leave an optional tip.

The problem is that you might not be eligible to use the Pay feature. Not to mention that the maximum cash limit is $150 each day or $500 max in a pay cycle.

The Pros

- No membership charge

- No advance fee

The Cons

- Limited to $150 a day or $500 in a pay cycle

- Need to have a bank-approved debit card

- Have to download the Branch smartphone app (everything is done on the app)

- Remote employees aren’t accepted

5. Even App

The Even app lets you request an advance of up to 50% of this month’s paycheck in advance! The catch is that you must work for an eligible employer. And, the amount you can advance each month can change drastically.

While this “Instapay” service is technically free, to access it, you will have to be an Even Plus member. This will cost you $8 a month.

The Pros

- Interest-free advances

- Get your money instantly

- Offers budgeting tools

- Great reviews

The Cons

- Your employer must be eligible

- $8 monthly membership fee

- No employer list so you can’t check if you’re eligible

- Only advance 50% of the money you’ve earned thus far

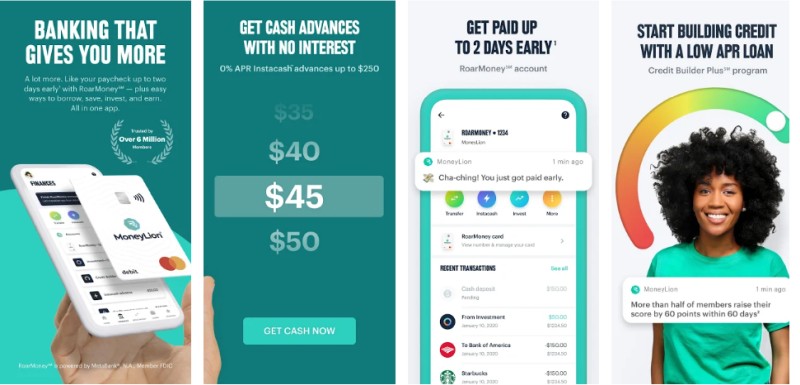

6. MoneyLion

MoneyLion allows you to get your entire paycheck 2 days early. This might not seem very helpful but those last couple of days in the month can seem like a lifetime when you’re about to swallow your overdraft.

On top of this, they operate a 0% interest with no credit check either so pretty much anyone can use their service. Plus, they can automatically invest your money and notify you when they have advice for you.

The Pros

- Get your money the same day

- No credit check

- TransUnion credit score each week

The Cons

- Customer service seemingly unreachable

- Technical difficulties

- $19.99 membership fee

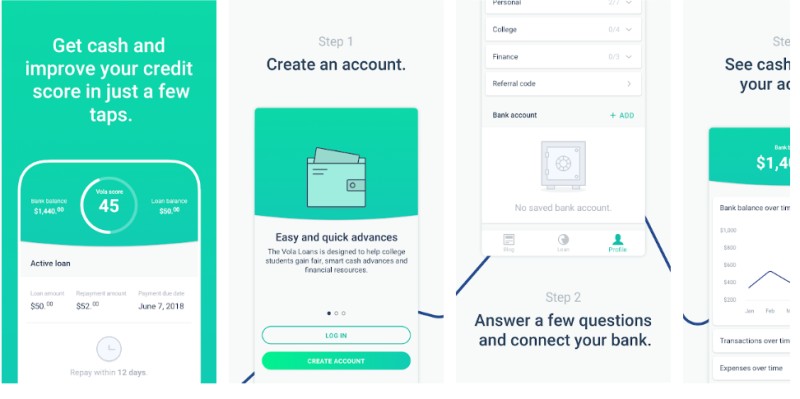

7. Vola Finance

After you have connected this app to your bank account, Vola will keep an eye on everything to ensure you manage your money better. Yep, this includes budgeting and saving.

As soon as your account hits $35 or less, the app will send you a notification. Then, you can request an advance of up to $300. The best aspect here is that you get the money instantly.

The Pros

- Financial tools and resources available

- Budgeting and saving advice

- Alerts you when your balance is low

The Cons

- Can only borrow up to $300

- Must have an average balance of $150 or over

- People have reported technical issues with the app

- Have to sign in to the bank to see membership tiers

8. DailyPay

DailyPay is another app which bases your benefit on the work you have already done. It’s only offered through certain employers but if your company is eligible, you can get instant access to your earned wage.

You don’t need to pay to use the service. Plus, it is compliant with all labour laws across the entirety of the United States of America.

The Pros

- Free service

- Complies with all labor laws in every American state

The Cons

- Based solely on the work you have already done

- Multiple negative online reviews

9. PayActiv

PayActiv prides themselves on offering a foolproof solution to avoiding overdraft fees, high-interest loans, and late charges.

You get instant access to the money you have already earned — even if it’s ages away from payday. Of course, like with all of these paycheck advance apps, you must work for a registered, approved employer.

The Pros

- Early access to payment for the work you’ve done

- Helps you avoid overdraft, late, and interest fees

The Cons

- Must work for a registered employer

- Can’t advance more than you have made thus far

10. FlexWage

Again, this is all about employer-sponsored financing.

You get on-demand pay that is not a loan. Instead, it aims to improve employees’ satisfaction and quality of life by ensuring they never have to pay overdraft fees.

The Pros

- On-demand pay

- Offers an option to replace paper paychecks

- Easily track your money

The Cons

- Must work for a registered employer

- Only get what you’ve earned

11. TapCheck

TapCheck gives you around the clock access to the money you have earned before payday. With these guys, you won’t have to wait for your money again. Yep, that means no more living paycheck-to-paycheck. And, you won’t be stuck if an emergency strikes.

The Pros

- 24/7 access to your money

- Cover emergency costs with ease

- Clean interface

The Cons

- Have to work for an approved employer

12. Solo Funds

SoLo Funds allows you to borrow money from your friends and pay them with “tips” rather than a scary interest rate. However, you need to be careful since these tips can be sky-high (you don’t want to pay as much as you would for a payday loan).

The maximum amount is $1,000 and it’s incredibly simple to do. You’ll have to describe why you need the money but that is easily done!

The Pros

- No interest

- Repayment extensions allowed

- No credit check

- If you can’t pay it back, turn it into a gift

The Cons

- Not guaranteed to find someone willing to help you

- Short terms

- Tips can be expensive

- Collections are reported to credit bureaus so if you can’t repay, it’ll damage your score

Leave a Reply