Fortunately, there are many options for folks who want credit cards without the typical hassles of filling out lengthy application forms, waiting for weeks to hear back from the issuers, and building credit by using the cards responsibly.

One of the niche leaders is the Arro Credit Card. With an introductory interest rate of 16% that goes down over time if you use the card responsibly, low annual fees, and no deposit, the Arro credit card and personal finance app are winning converts.

Arro uses your bank data, not your credit score, for approval decisions. Plus, applicants get a decision in minutes, and the card can help boost their credit because Arro reports to all three bureaus.

However, for different reasons, people want to have alternative options similar to Arro Card for building credit or for other personal finance features.

Here are how 10 similar apps stack up. The list below is in no particular order.

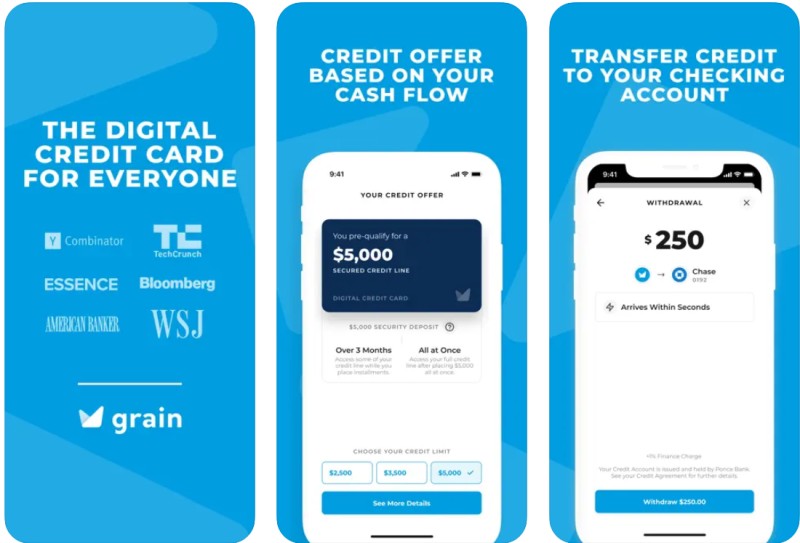

1. Grain

The Grain app (available for both Apple and Android devices) lets users build their credit and access needed cash at rates much lower than typical payday loans or cash advances on traditional plastic cards.

You get a virtual credit line after applying and being approved. The money goes straight to your personal bank account. That’s why it’s called a “virtual” credit card.

There are no credit checks, but the app reports to all three bureaus as if it were a standard credit card, and you can boost your current credit score if you use it responsibly.

There are some customer support complaints on record. Also, the app comes with transfer fees, and some users must pay a security deposit.

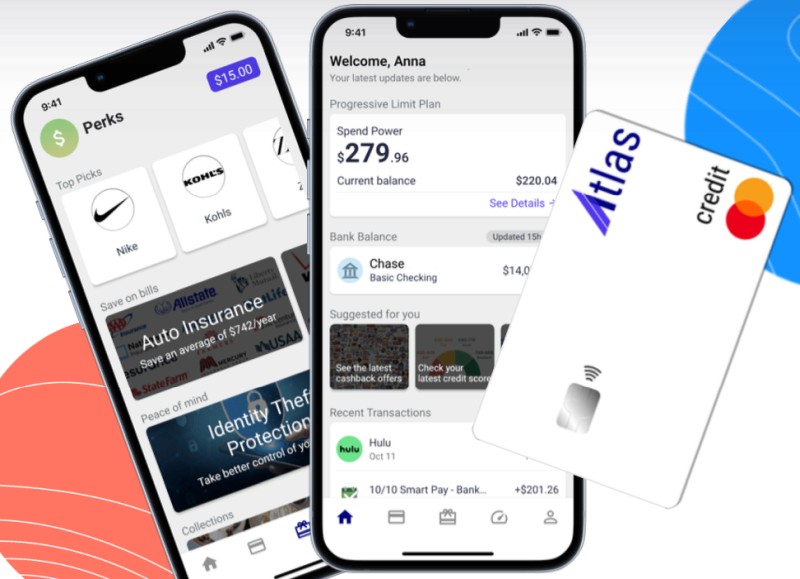

2. Atlas Card

The Atlas card comes with plenty of financial incentives for prospective users. There’s a 0% APR, adjustable and safe spending limits that change over time, very high approval rates, an average savings of $1,850 per year based on the average user’s habits, no income required, and no credit history required.

Note that the Atlas card has a 5 times higher approval rate than traditional plastic cards.

The Atlas card is designed to grow with users as their finances become more stable.

Additionally, applying and getting approved takes less than two minutes. You can connect the app to your current bank for an affordable spending limit.

And, if you set up autopay, it’s possible to avoid worrying about accumulating a substantial balance. Atlas reports to all three bureaus.

3. Kikoff Card

With no required credit score, no APR, and a credit line of $750, the Kikoff card is popular with many consumers.

It’s like getting the upside of a banking service with a credit-building feature as a bonus.

The $750 amount is the only line offered, and the account is used as a credit card with no interest.

However, you can only purchase from the company’s online store, with a monthly fee of $5.

Kikoff reports to Experian and Equifax, while all cardholders can track their progress with a VantageScore rating built into the app.

You don’t have to link your bank account; there’s no credit check. Kikoff is a decent option if you need to ramp up your current credit score.

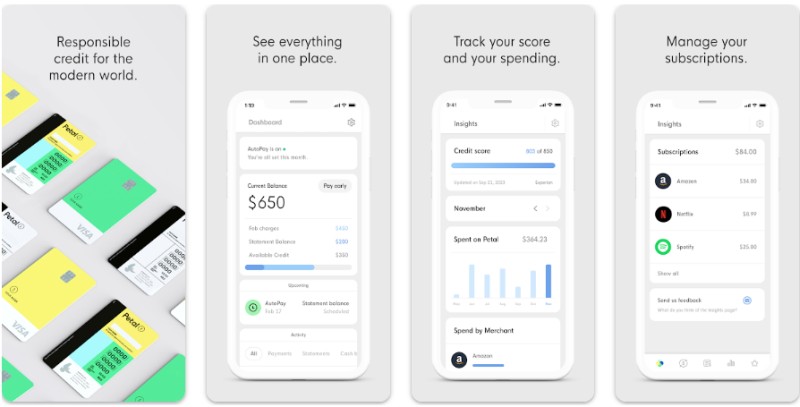

4. Petal Card

The Petal Card works differently than many of its competitors. The company uses your financial behavior history, not your credit score, to determine approval.

They look at spending habits, savings history, and income, among other things. Even if you have low credit scores or a thin credit history, it’s possible to get approved quickly.

The mobile app is user-friendly, offering real-time tracking of cardholders’ spending.

There are no annual fees, and Petal Card has a competitive variable APR. The company wants to assist users via financial education.

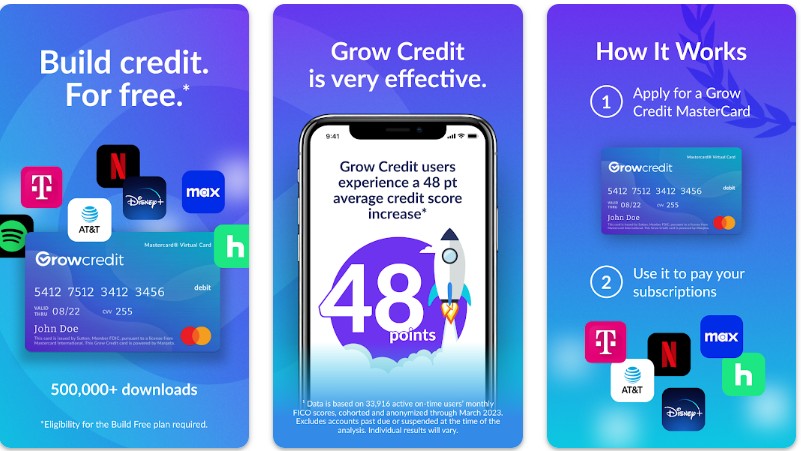

5. Grow Credit

The Grow credit card app has nearly a half-million downloads, and its goal is to assist users with credit-building via their subscriptions.

There are no credit history requirements, but the card reports to all three bureaus. After applying and getting approved, users link their bank accounts and add subscriptions to providers like Hulu and Netflix.

There are more than 100 subscriptions to choose from on the app. All subscriptions are billed directly to the Grow MasterCard. The company uses auto withdrawal to bill you monthly.

There’s no hard pull for applying, so you don’t need to worry about taking a score hit just for signing up for a Grow credit card.

There are several plans, with spending limits of about $200 to $600, and fees are between nothing and around $12 per month.

6. Sequin Card

Sequin is an oddity in the credit card app niche because it’s a hybrid between a credit and debit card.

While there are zero monthly fees or interest, it does help you build credit by reporting your on-time payments to one bureau without disclosing your credit utilization. You can set daily limits, and there’s no credit check to join.

Because it’s connected to your bank account, you never have to fund Sequin directly or take money from it.

Sequin provides you with funds like a credit card but immediately withdraws that amount from your account.

Only reporting to Experian, Sequin can help users build their credit scores with on-time payments without impacting their credit utilization rate.

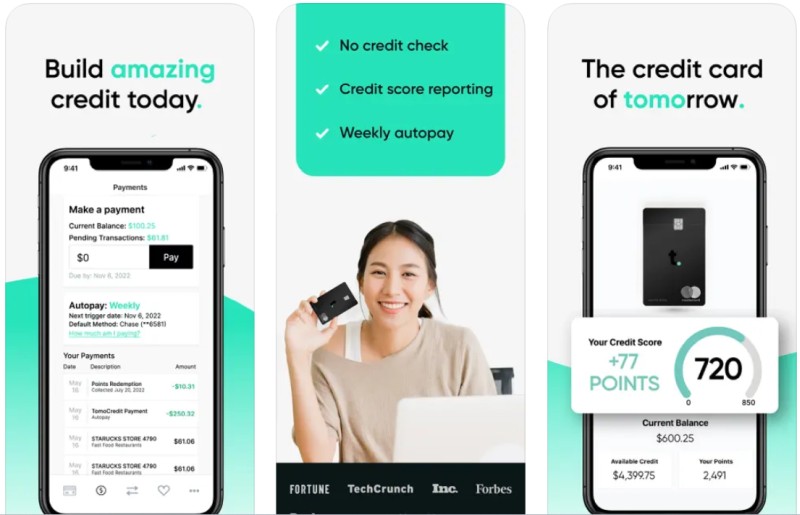

7. Tomo Credit

The creators of the Tomo credit card set out to give a chance to folks who have weak or thin credit histories but who do have income.

After you provide information about your assets, savings accounts, and checking balances on Tomo’s application, they’ll decide on approval based on your potential credit limit based on that information instead of a credit rating or history.

In addition to reporting to all three bureaus, users can leverage the card to build their credit over time with on-time payment and responsible spending.

Tomo is a charge card, meaning that with zero interest, cardholders must pay off balances in full when they receive their monthly bills.

You never carry a balance on Tomo, so deciding whether this type of arrangement is what you’re looking for and if it fits your financial situation is essential.

8. Credit Genie

Credit Genie is a cash-advance app that gives new users up to $100 without a credit check.

But you need a linked banking account to access the app’s features, which include, in addition to the cash-advance perk, products that can help you manage your finances. To maintain high security, the company uses Plaid.

To get cash, you cannot have a joint bank account, must have an account that has been active for the past 90 days or longer, receive direct deposits (two of them at least) per month, and have at least $750 worth of direct deposit activity within the past 90 days.

Credit Genie uses your repayment behavior to raise or lower the cash-advance limit. Some customers reported that the initial limit dropped substantially after the first advance.

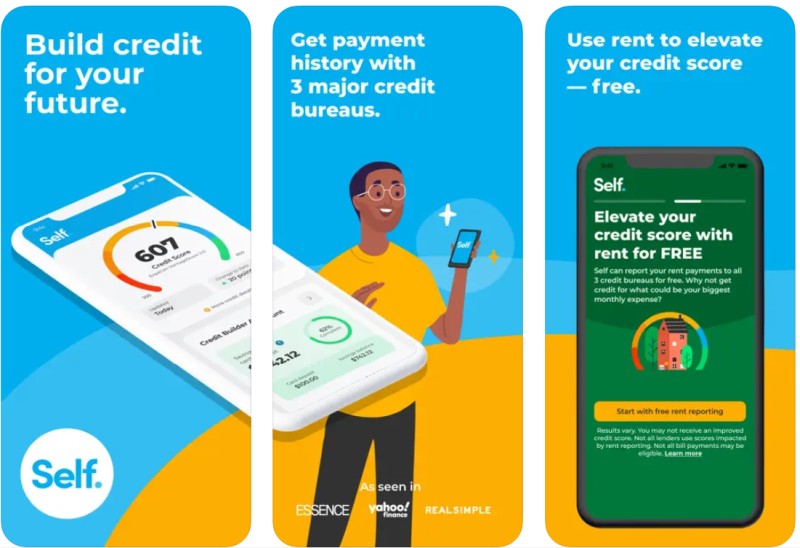

9. Self

Self is a credit-builder loan app with features of a credit card that came onto the market in 2014. It’s designed for folks with no or little credit history.

The company claims that most users, on average, boost their credit scores by 49 points after the two-year term of usage for the app.

Available in all US states, various payment plans range from a low of $25 per month to a high of $150.

They all last for two full years. The card reports to all three bureaus, and there are no hard credit pulls for applicants.

After users make three on-time payments on the secured card, they can convert the credit-builder loan to a secured Visa card.

Still, you must pay at least $100 to the connected credit-building account during that trial period. The APR is relatively high, at about 28%, with a yearly fee of $25.

10. Chime Mobile Banking

The popular banking app works to maintain financial safety with features like overdraft protection, early paycheck receipt for those who use direct deposit, and zero monthly fees.

In short, Chime is not a bank but a fintech company. The card is officially called the Chime Visa Credit-Builder card and is issued by Stride Bank.

Cardholders can use it wherever Visa is accepted, which is almost everywhere. Holders get daily balance alerts and instant card blocking if they sign up for TFA (two-factor authentication).

If you’re eligible, you’ll get no-fee ATM withdrawals and $200 worth of overdraft protection.

There are zero foreign transaction fees, minimum balances, and monthly fees for account maintenance.

Workers can receive access to their paycheck amounts up to two full business days early.

The card’s Credit Builder feature can help boost your FICO score by as much as 30 points. There is no credit check to apply for a Chime card, zero annual fees, and no interest.

Leave a Reply