Buy-now-pay-Later (BNPL) apps are currently among the hottest items for consumers who like to save money on a wide range of items. For example, Katapult users can take advantage of lenient lease-to-own arrangements.

The Katapult app gives financial freedom to buyers who don’t have credit cards or wouldn’t be able to borrow for major purchases.

They can make periodic payments, weekly or otherwise, without worrying about credit checks.

Katapult users with no credit history or low scores can shop at stores like Motorola, Sears, Wayfair, and dozens of others.

Formerly called Zibby, Katapult opens the doors to ownership of big-ticket items like furniture, tires, laptops, etc.

For instance, consumers who need a gaming setup that costs $3,000 can sign up with Katapult and choose a suitable lease-to-own payment schedule.

Approval for the app takes less than 30 seconds, and millions have already used it to acquire all sorts of goods.

There are many other BNPL apps that people use to acquire their favorite goods. So, what are the details on 10 other apps that are similar to Katapult? Here’s the rundown.

1. Affirm

The main characteristic of Affirm is that it serves as a viable alternative to traditional plastic for consumers who don’t want to use cards or can’t get approved for them.

All the financing options are clear and user-friendly on the app. Affirm is based in the U.S. and offers a wide array of repayment arrangements. Most people select a payoff plan from several months to a few years.

All interest rates are displayed before buyers make their purchase decisions. The creators of Affirm designed the app to encourage informed and savvy financial behavior.

Currently, users can select from hundreds of merchants, which include some of the world’s largest retail establishments as well as very small sellers.

Expedia, Walmart, Target, Samsung, and Amazon are just a few of the stores Affirm devotees can choose from.

2. Klarna

Consumers who use the Klarna app can choose to divide up the cost of items into four payments. There is no interest, and payments occur every two weeks.

Basically, it’s a non-credit-card way to buy goods on an 8-week, same-as-cash payment cycle. Klarna partners with merchants from international markets. When you buy items from a partner’s website, the transaction is quick and uncomplicated.

Plus, should there be a glitch of any kind during the ordering or delivery process, Klarna will make it right. The interface is clean and easy.

There’s even a special “Pay Later” choice for consumers who want to delay their payments for as long as 30 days. The app was developed by a Sweden-based fintech corporation and has enjoyed great success in a competitive market.

3. Sezzle

Billing itself as the leading BNPL app that offers users a chance to build their credit, Sezzle has a simple and user-friendly interface.

Over a six-week timeline, buyers can divide their payments into four installments. Designed and marketed to budget-savvy individuals, Sezzle is known for being interest-free when users make on-time payments and for its transparent way of displaying fees.

The technical side of the app is excellent, as it integrates with all partners’ merchant sites quickly and seamlessly.

There are many retailers and product types to choose from. The app is flexible, payments are predictable, and the whole experience is suited for folks who like to pay close attention to their personal budgets.

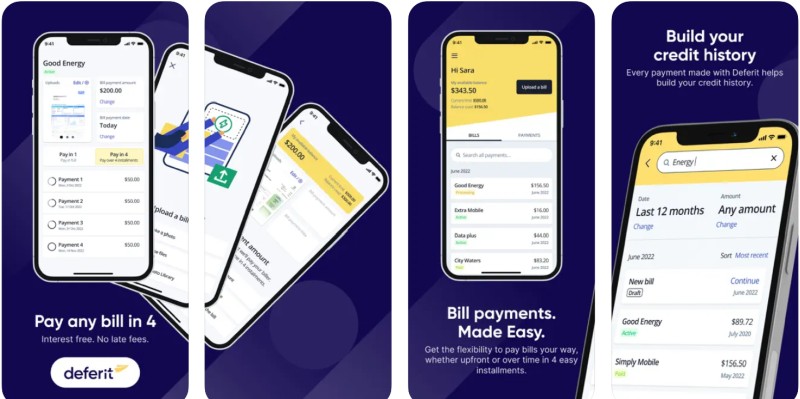

4. Deferit

Deferit’s app is a workhorse. It lets users pay in four installments with zero interest. They can upload bills, decide how much they wish to pay, and make a purchase all in one process.

But there’s much more to Deferit than BNPL functionality. With more than a half-million U.S. users, Deferit assists people with bill management via deferrals, subscriptions, and negotiation on various services and goods.

It’s actually a comprehensive way of dealing with personal budgeting that has no charges, late fees, or interest. The whole idea of the app is to use standard BNPL concepts for everything a consumer spends money on, not just retail purchases.

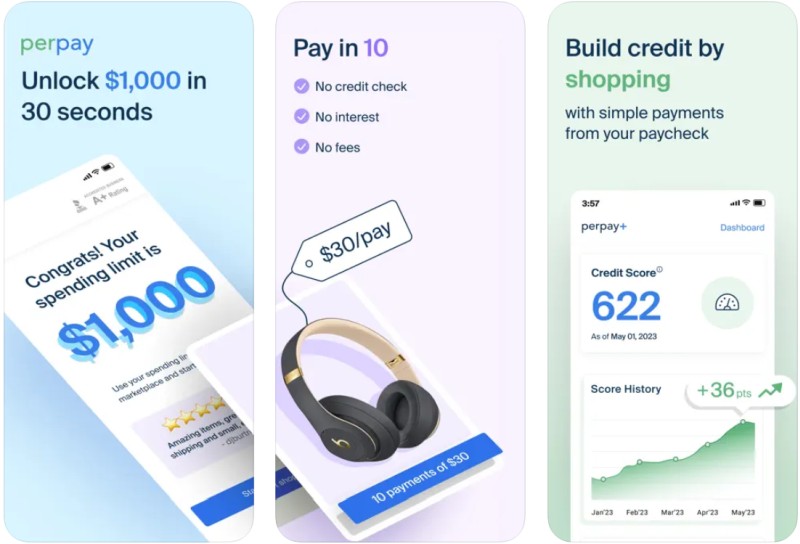

5. PerPay

PerPay is a unique member of the BNPL group of apps because it helps people manage their personal finances. Without incurring interest, users can make all kinds of purchases.

The focus is on “financial wellness,” and there are plenty of tools for budgeting and controlling spending, along with educational resources.

The interface is user-friendly and fully transparent. The creator built PerPay as an all-in-one app for consumers who want to buy their preferred brands, build credit scores, pay over time, and learn how to navigate the personal budgeting process. The average user’s credit score can go up about 36 points.

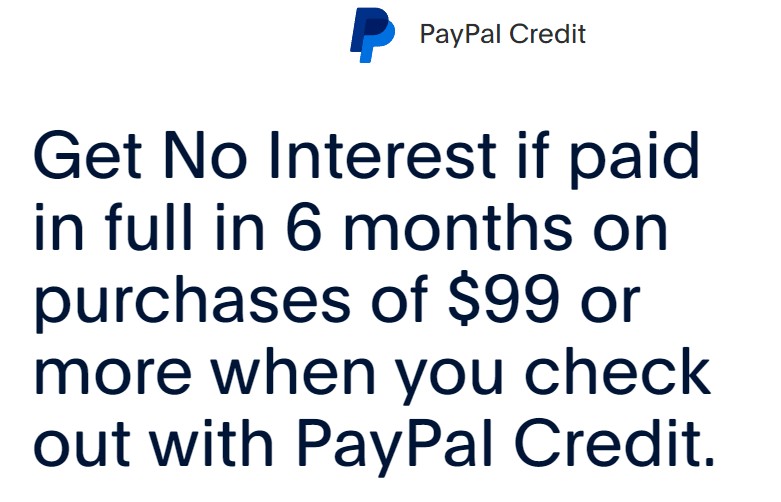

6. PayPal Credit

Even though PP Credit isn’t a traditional BNPL app, it is so much like one that we included it on this list. The app gives users a chance to pay for almost anything within a time window of six months.

On purchases greater than $99, there is no interest for those first 180 days. However, if you don’t pay the full balance within six months, PayPal Credit will charge you interest from the day of the original purchase. There are monthly minimum payments, and the APR is relatively high, at just over 29%.

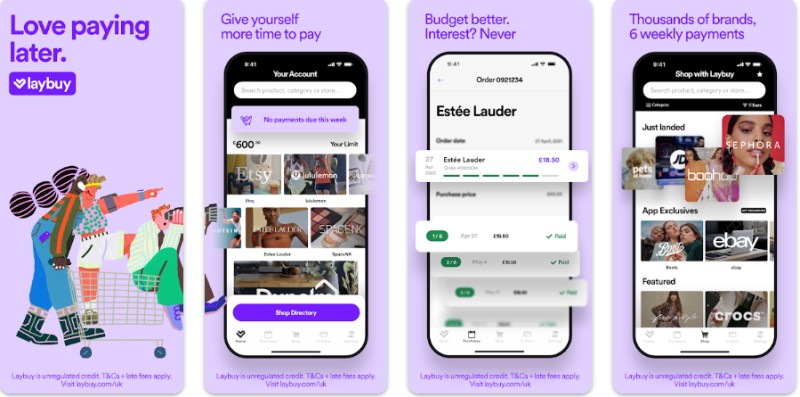

7. LayBuy

LayBuy works with thousands of retailers and gives users a simple way to make online or in-store purchases.

With one login, you can pay online or use the personalized barcode on your phone to buy items in person. With no credit checks and full flexibility, consumers can pay via six weekly installments.

It’s designed for people who like the idea of quick payback on retail items. The app shows users how much credit they have left at any time, and there are no financial penalties for making early payments or payoffs.

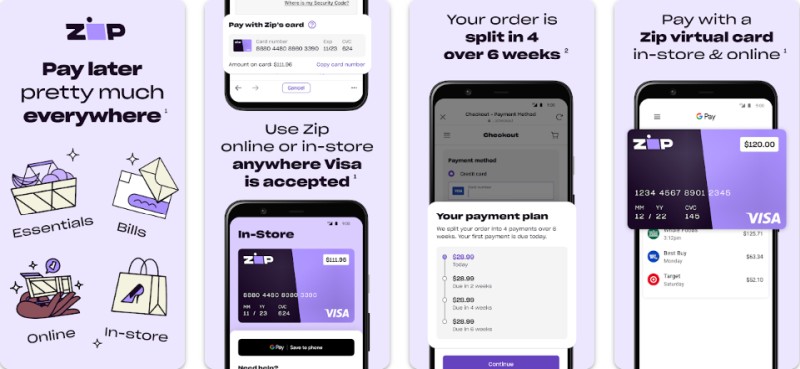

8. Zip

Use Zip in-store or online. Many people remember Quadpay, but the company changed its name to Zip and added many features to its popular BNPL app, like total financial flexibility with a four-installment, six-week payment arrangement.

There are literally thousands of in-person and online merchants available via the app. There are no lengthy forms to fill out, and applicants get an immediate decision when they inquire.

There are pay-later and pay-monthly options, as well as variations called Zip Pay and Zip Money, the latter of which is like a line of credit you can use to set up extended repayment on big-ticket goods.

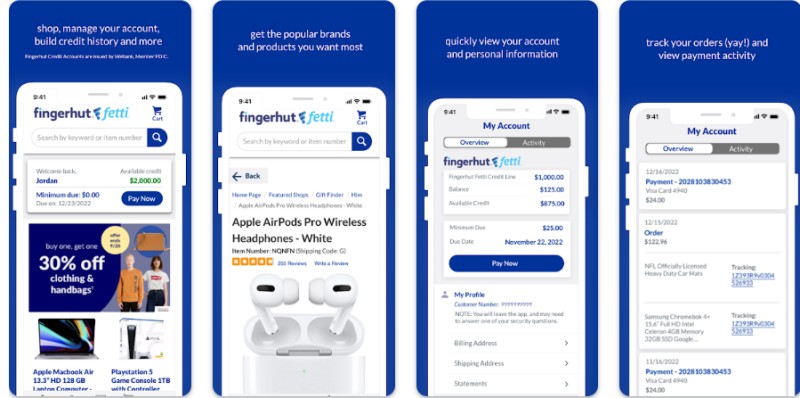

9. Fingerhut Mobile App

Use a standard password login or choose fingerprint verification with this versatile app. Along with standard BNPL functionality, the Fingerhut Mobile assists users with credit-building or rebuilding, offers a massive range of products, and comes with low monthly payments.

It’s easy to see your available remaining credit at any time, track orders, set up recurring payments, view all past transactions, get access to special promotions, and shop for goods from some of the world’s largest retailers.

10. Apple Pay Later

Apple’s simple BNPL app is a no-frills way to buy things. There are no fees or interest, and it’s easy to use with any seller who accepts Apple Pay, which means millions of places to shop.

For purchases between $75 and $1,000, users can split payments into four installments or hit the “Pay Now” button.

The installment system is a six-week arrangement, and the first payment is due at the moment you buy something.

Then, you’ll make the remaining three payments over the following six weeks, at which time the agreement is paid in full. To get started, set the app up on your phone and begin shopping.

Leave a Reply