When Ryan Browne was approached about profiling the meteoric rise of the “buy now, pay later” movement for the cable business channel CNBC, he quickly discovered that this industry took very little time to flourish. By 2021, it had become a $100 billion marketplace.

What reasons does Browne cite to explain this growth? The confluence of an already-established network of point-of-sale loans and layaway plans, the onset of COVID, plus the ease with which consumers adapted to this alternative buying method.

Are there risks? That depends upon one’s propensity for overspending, which can lead to debt, but for responsible consumers, buy-now-pay-later plans are a delight—-especially beloved by millennials and GenZs.

Most of these apps don’t require hard credit checks, a boon to folks trying to boost their credit ratings, and they are more sensible than payday loans.

If you’ve yet to try Four app–or any of the competitors profiled here– perhaps it’s time to do so.

In this article we’ll list and discuss 10 alternatives to “Four” app as buy-now-pay-later purchasing options.

What is Four app?

Before discussing similar apps, let’s first talk briefly about “Four”.

It’s a pioneering entity that allows you to order items you need and want, receive your goods quickly and pay for them over time by using a pre-determined repayment schedule.

Perks include no credit checks and no interest, and the one-click checkout function won’t require you to fill out lengthy credit application forms.

Named for the number of payments customers make to repay their bill, the Four app also promotes retailers who are receptive to interest-free payments, and since it’s easy to repay these charges via credit cards, debit cards, Apple Pay, Google Pay, and more, shopping is effortless.

People might want to use other apps as well so knowing about alternatives is a smart move so you know all available options out there.

Let’s now discuss 10 apps like Four below. The list is in no particular order.

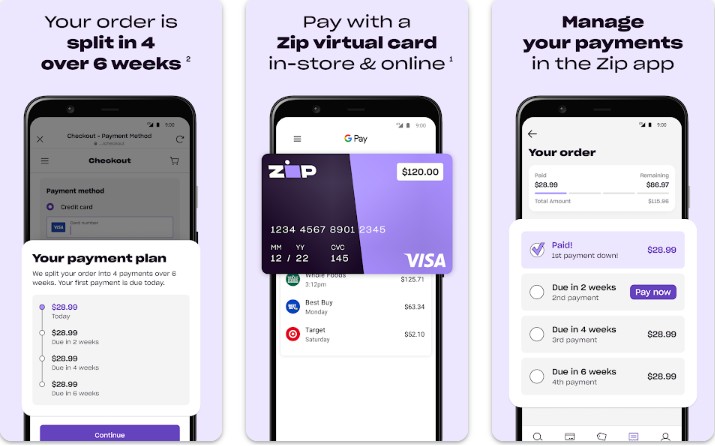

1. Zip (Quadpay)

The name of this app may have changed from Quadpay to Zip, but developers insist that this tool continues to give “savvy shoppers more freedom and flexibility to buy now, pay later.”

Like Four, consumers pay their bill in 4 installments within a 6-week period. Marketing itself as “the smarter way to find great deals,” one can get an instant okay.

Use Zip online or at retail stores once you download it to your Google Pay or Apple Wallet.

Minimum purchase must be at least $35, but you can track your spending and transaction history plus change or update your account at any time.

There’s a $4 installment fee as a prepaid charge, $1 of which is added to each of your four payments. Read the small print. You could be subject to a credit check, and be advised that Zip can only be used for purchases made in the U.S.

2. Paypal Pay in 4

You already recognize the name and logo, so if you tend to prefer established brands, Paypal Pay in 4 may give you the most amount of comfort.

You’ll be asked how you want to repay the money you spend after using the Paypal website to shop trendy brands.

You can “Pay in 4” via interest-free, bi-weekly amounts after spending between $30 and $1500, or you can spend more and work out monthly repay plans that won’t require a down payment.

Further, you are given 6, 12, or 24 months to satisfy your debt. There are no sign-up charges or late fees attached to either repayment plan if you’re diligent about managing debt.

Be cautious though: If you take the monthly option and incur between $199 and $10,000 in debt for making purchases, you could be assessed interest rates that range between 9.9% and 29.99%!

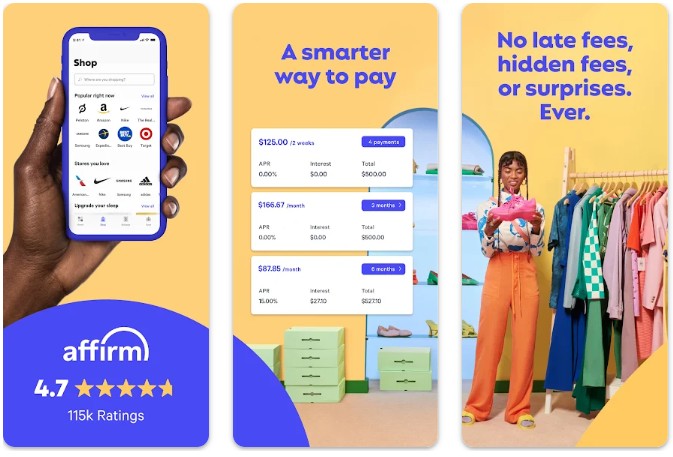

3. Affirm

Positioning itself as the premier stress-free, flexible payment option, The Affirm Card is your conduit to the realm of buy-now-pay-later, offering you access to “exclusive deals and rates as low as 0% APR.”

Not only will this app hold you accountable by helping you manage your account and make payments, but unlike some competitors, Affirm gives you the opportunity to open a high-yield savings account with no minimum deposit.

Users are very complimentary. They find Affirm simple to use yet there is no impact on one’s credit score.

As a planning tool, Affirm receives kudos for notifying users of payment deadlines and keeping tabs on open balances. Use Affirm responsively and you could be offered larger lines of credit that come with longer payback schedules.

4. Afterpay

If you’ve been checking out each of these apps in order, you likely noticed a lot of repetition, but in sleuthing out differences, we offer a few cautions if you select this as your buy-now-pay-later option.

Afterpay Android app on the Google Play store states that your data isn’t transferred over a secure connection and this is not a good practice for a financial/shopping app.

I don’t know if this was stated by mistake from the developer, however you should be cautious.

That stated, you can download this app to gain access to thousands of stores and brands and reimburse your shopping bills over 4 installments that are interest-free and you won’t run into fees as long as you make payments on schedule.

Afterpay makes a concerted effort to add new retailers to its directory, but keep this in mind: Despite complimentary customer service reviews from users, some of them ran into technical problems (e.g., glitches, lags, and freezes) while using this app.

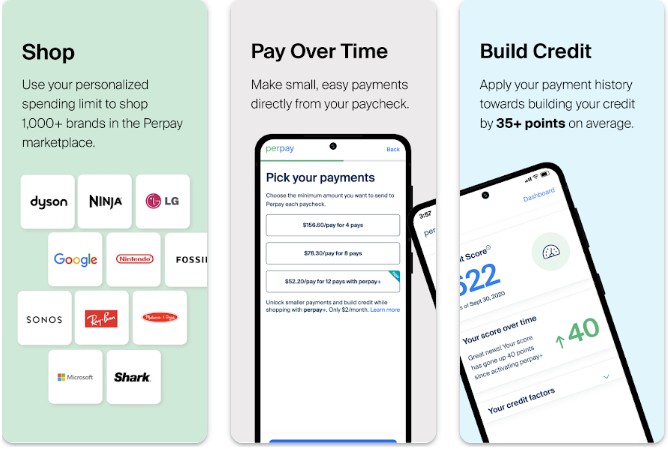

5. Perpay – Shop and Build Credit

Perpay has a slightly different marketing pitch from competitors on this list because they emphasize rebuilding iffy credit as a major perk.

Similar in terms of having access to popular brands and the opportunity to pay charges over time, this app claims to have 6+ million members who enjoy zero fees and interest and each of whom is offered $1000 in “spending power.”

Pay your bill directly from your salary or arrange a different method. According to statisticians, no app is easier, simpler, or more transparent, and loyal customers say that their average credit score improved by 39 points as a direct result of utilizing Perpay.

If your credit score numbers could stand improvement, this could be your solution.

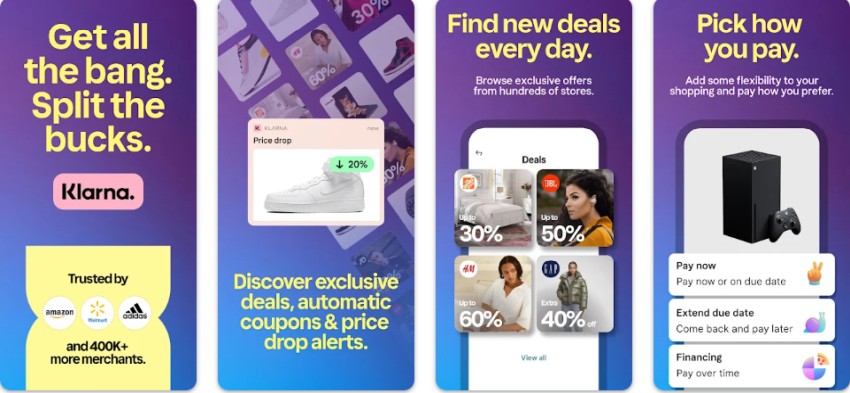

6. Klarna

If you use an Android or Apple device, avail yourself of Klarna’s benefits, including 4 interest-free repayments paid in 2 week intervals to keep the account in good standing.

Klarna can be used for goods and services and there are plenty of complimentary reviews from satisfied users. It is also one of the most popular buy-now-pay-later services out there.

Browse deals (new items are added daily) and sign up for the Klarna Rewards Club where you earn 1 point for every dollar you spend.

A $5 welcome reward is yours when you place your first membership order. Would you feel more comfortable with a credit card in your wallet? Apply for one—-minus the interest charges–as you pay your balance down.

Customers are complimentary about Klarna’s delivery tracking system and hassle-free returns, plus “price drop alerts,” so if you’ve got your eye on something that’s too expensive, waiting could be rewarding.

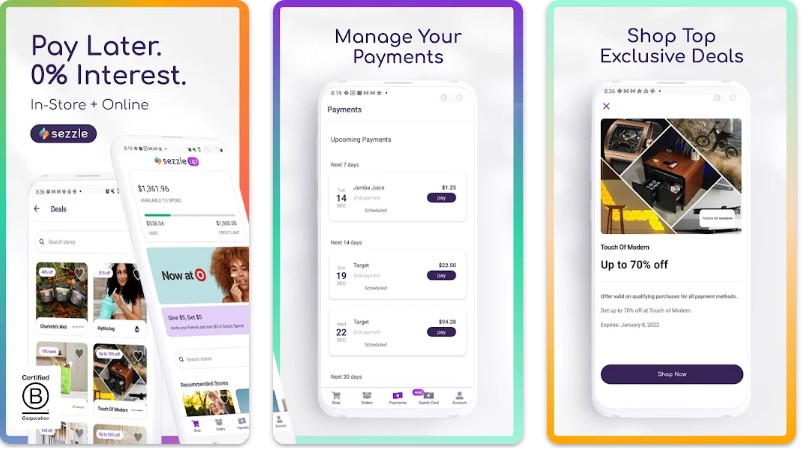

7. Sezzle – Buy Now, Pay Later

While Sezzle positions itself as a Buy Now, Pay Later service, this app also offers a Premium subscription service ($11+ monthly) which allows you to purchase from other big brands such as DoorDash, Lowe’s, Hotels.com etc.

There’s a disclaimer that suggests that “Data privacy and security practices may vary based on your use, region, and age.”

Further, you could find a spending ceiling change without notice. One user reports a major drop in her credit score when she began using Sezzle and you’ll need to upgrade to Premium to buy gift cards and accrue loyalty points, so proceed with caution and make your due-diligence if you pick this buy-now-pay-later option.

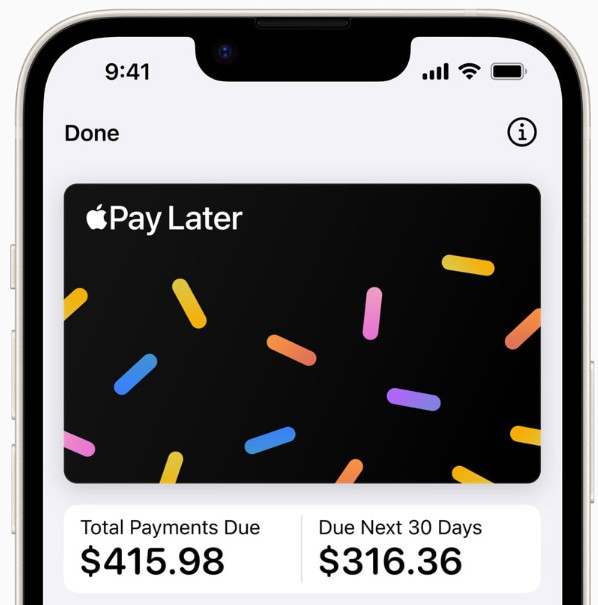

8. Apple Pay Later

When Apple took a page from the playbook written by the credit industry’s first buy-now-pay-later model, the company stuck to the “4 payment/0 interest/0 fees” structure, so you’ll have to dig deep into the company’s marketing materials to find differences.

You’ll have up to 6 weeks to make 4 payments and once you’re established, myriad perks kick in that include tracking service and loan management.

Apple Pay Later won’t impact your credit score but you’ll need an iPhone or iPad when you shop.

Subscribers receive notifications via the Wallet app and are warned ahead of time that credit cards won’t be accepted to help wrangle a balance to the ground.

Designed with an emphasis on privacy and security, purchases using Apple Pay Later can be authenticated using Face ID, Touch ID, or passcode and all underwriting is handled by Apple Financing LLC and administered through Goldman Sachs’ Mastercard installments program.

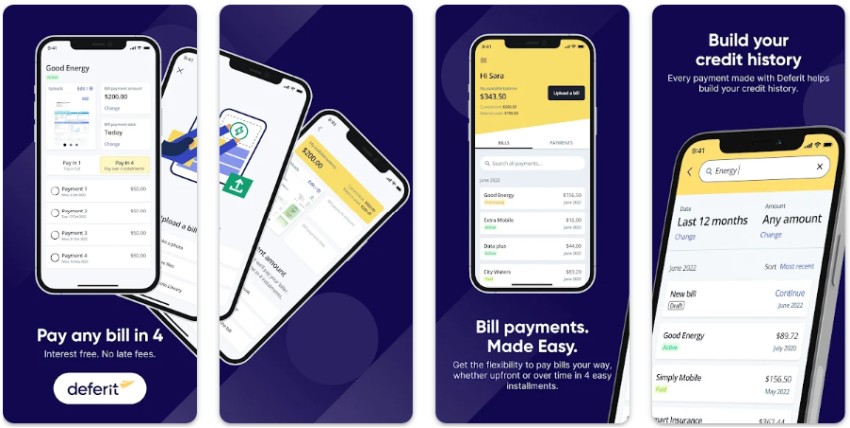

9. Deferit: Pay bills in 4

This app is different from the rest in this list. You can use it to pay bills over time (in 4 installments) instead of shopping like the other apps above.

The financial company backing this application claims to have hosted 100,000 downloads thus far as interested subscribers are attracted to the app for paying their bills in installments.

You’ll be required to have an Android or Apple device to upload a photo of a bill, a screenshot or file with details of your bill.

In each case, you tell the app how much you want to send to the creditor and then choose from the payment plans that you are given.

Deferit works differently from competitors. It pays the full amount of your owed bill upfront so you’re technically re-paying this financial resource.

This app sounds like a good way to learn to manage debt since the user has more control over amounts than competitor products, so if this is your goal, you may wish to give Deferit a go.

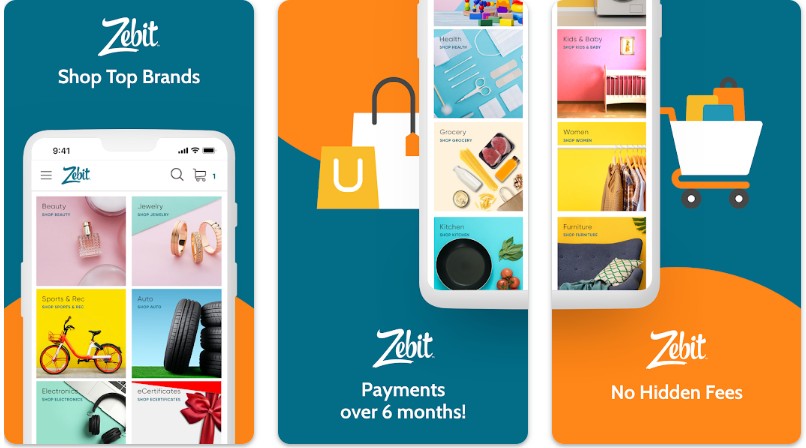

10. Zebit

If you use an Android or Apple device, this app belongs in your short list. You’ll be made privy to thousands of products, orders are shipped immediately, and you pay later with no hidden fees.

Folks with decent credit can qualify for up to $1500 with a 6-month repayment schedule.

Further, you’ll know where you stand from the moment you apply. Once you download the app, you’ll receive a specific spending limit and once you’re approved, a down payment is required.

Most Zebit subscribers are given “spending budgets” of between $750 and $1500 once personal data is reviewed.

If you’re financing a $1000 item, you’ll make a down-payment of $300 and the remaining $700 is financed at 0% APR for the next 6 months.

Importantly, Zebit says not all customers will be approved for credit, so keep that in mind if your credit scores are low.

Resources

https://www.cnbc.com/2021/09/21/how-buy-now-pay-later-became-a-100-billion-industry.html

Leave a Reply