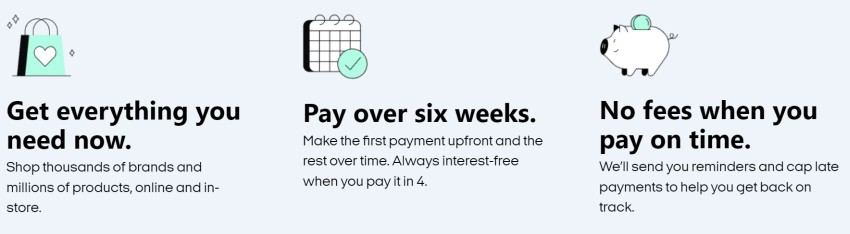

The hottest concept in retail, both for online and brick-and-mortar stores, in the 2020s is BNPL, or “buy now, pay later.”

The attraction for most consumers is the flexibility, which offers several benefits at once.

Not only can buyers get items immediately without full payment, but they can break up the financial pain of acquiring items by spreading payments out over multiple weeks or months.

The budget-friendly tactic was a staple of online stores like Gettington and now people are looking for alternative shopping solutions since Gettington stopped its operations.

The following 15 sellers all maintain high-traffic websites and offer buyers the chance to get the goods in their hands before paying for them in full.

Here’s a quick rundown of stores and sites similar to Gettington that offer flexible payment options.

1) Stoneberry

Using Stoneberry Credit, customers can make purchases and their payments can be as low as $5.99 per month.

However, each buyer must be approved for the Stoneberry account before they can take advantage of BNPL options.

But, the application form is very short, does not affect credit scores, and is approved fast for those who qualify.

Stoneberry sells appliance, electronics, furniture, and many more kinds of goods. In addition to BNPL, the company offers exclusive deals to regular customers.

2) Amazon Pay

Amazon is the largest retailer, so it only makes sense they’d team up with others to offer a wide variety of payment plans for buyers.

Through BNPL services like Affirm, Amazon Pay lets customers choose a pay-later arrangement during checkout.

It’s a standard monthly payment plan, but those who use Citi Flex can get a 0% APR for up to 48 months. With Affirm, buyers can select goods priced above $50 and make regular monthly payments.

3) Wayfair

Major retailer Wayfair carries a vast collection of home goods, furniture, and more.

They offer a large variety of BNPL plans because they team up with third-party services for financing, like Klarna and Afterpay.

The installment methods tend to be four payments with no interest over a period of two months.

Payments are made every two weeks by purchasers to get the benefits of no interest or additional charges.

4) Zebit

Zebit is primarily for folks who have not-so-great credit, but others use them for their 25-35% down payment plans that split the remainder of the price into 6-26 installments with no interest but which are spread over six months or less.

Not all orders are approved because Zebit does a credit evaluation on each purchase. There are no traditional credit checks.

5) Abunda

Also called Shopabunda, the e-commerce platform is more of a gateway or platform than anything else.

For example, it works exclusively with Amazon and gives users a wide range of BNPL options. Amazon lists millions of goods on its site.

Customers can leverage the power of BNPL platforms like ViaBill, Klarna, and Acima Leasing to acquire goods on the Abunda platform.

Arrangements vary but tend to follow the standard installment plan of two or more payments per purchase.

6) QVC

The popular TV network has expanded into online sales with many variations of pay-later arrangements. Their Easy Pay system gives buyers several months to pay for items with zero interest in most cases. Customers can use Easy Pay or the QCard, which is QVC’s proprietary credit card.

The site also accepts PayPal as a standard payment method. For shipped goods, the installment price includes sales tax, shipping charges, and the product’s price.

The grand total is divided by the number of payments in the agreed-upon installment arrangement.

7) Perpay Marketplace

Perpay operates a bit differently than many other online sellers. There are no fees for membership, and the company does not charge any late fees.

Additionally, there is no interest charge on the installment payments. All of which makes for a relatively straightforward, simple buying experience.

The company uses your latest verified pay stub to determine your spending limit. Then, most purchases can be placed on a no-fee, no-interest 12-month payment plan.

8) Ginny’s

When customers apply for a Ginny’s credit account, they gain access to a number of different BNPL options. One is the chance to pay as little as $10 per month on items priced at $100 or less. The program is similar to a revolving credit account with a retail store.

But Ginny’s gives its credit customers lots of extras, like enhanced buying power, super-fast account approval even with low credit, and the chance to earn a higher spending limit with on-time payments.

By selling electronics, home goods, and several other categories of items, Ginny’s has slowly built up a loyal customer base during the past decade.

9) Country Door

Like many BNPL arrangements, those offered by Country Door come with no fraud liability, monthly payments as low as $20, simple account set-up, and zero annual fees. The niche seller offers mostly home-oriented goods, like furniture and decor items.

There are multiple BNPL arrangements on their site, but most are set up to give customers four installment payments or standard revolving-style credit on the goods they purchase.

Decorating a home can be a costly project, so Country Door began offering payment arrangements to lessen the financial sting for homeowners who need items to complete a project but are happy to pay the bill in separate, timed installments.

10) Fingerhut

Fingerhut is another of the “old school” retailer on this list, but their marketing and sales methods are fully up to date.

Their online store offers many thousands of items in all sorts of categories, each one advertising the “buy now” price alongside an installment price. However, unlike many similar BNPL retailers, Fingerhut coaxes users into a credit card arrangement.

You must apply for Fingerhut credit and be approved before you can make any purchases.

While it is relatively easy to gain approval, even with weak credit, many of the items are priced higher than at other retail stores.

Fingerhut’s business model is to sign people up for their store credit cards, which are essentially like classic revolving lines of credit.

11) Flexshopper

People who like the idea of browsing among thousands of different consumer goods in multiple market segments enjoy purchasing from Flexshopper’s platform.

The company specializes in giving its customers weekly or monthly payment arrangements on a lease-to-own basis.

In other words, your lease payments all go toward the eventual ownership of the item you’re interested in.

In just a few minutes, potential customers can get approved for a Flexshopper spending limit as high as $2,500, which is an ideal solution for folks who have middling credit ratings. The company’s goal is to give people with so-so credit the chance to use installment payments to purchase the things they need.

12) Seventh Avenue

SA is one of the most successful online retailers. They offer BNPL arrangements that give consumers fast approval and monthly payments as low as $20.

There are no annual fees for using the SA BNPL arrangement, which is essentially a special credit-buying plan offered by the online and catalog seller.

The company’s product menu is highly varied and ranges from fashionable clothing to household furniture.

Consumers can spread their payments out, without interest, for several installments. One of the stated goals of SA’s corporate team is to make high-quality consumer goods accessible to as many people as possible.

13) Montgomery Ward

Montgomery Ward is one of the oldest major US retailers. One of the dominant catalog retailers in the last century, Wards has decided to build a massive online store for the new age.

They are now one of many companies that maintains a huge online store and offers flexible payment arrangements.

Because many of their products are big-ticket consumer items, like furniture or appliances, offering BNPL arrangements is one way to boost sales.

Consumers prefer to spread out payments when they make impulse and large purchases, and Wards specializes in higher-priced household goods.

The whole point is to minimize the financial impact of buying something like a washer, couch, or refrigerator.

14) Home Shopping Network with FlexPay

The Home Shopping Network has been around for decades. It started as a phone-in retail center that used television infomercials to generate business.

Nowadays, the TV side still exists, but the seller uses the powerful FlexPay system to make it easier for potential buyers to come into the fold.

The HSN television-based network has found success by offering installment arrangements. People who use it can select from a menu of different options, all of which are delayed installments of one type or another.

Not only is the customer experience seamless and fast, but it gives consumers of impulse goods less financial pain when acquiring a new item.

15) Afterpay

Users who purchase goods from Afterpay aren’t buying directly from a specific retailer. Instead, they’re routing their payment through a third-party service so that they can take advantage of a specialized BNPL arrangement.

The way it works is that Afterpay has in-place agreements with hundreds of merchants who agree to take, through Afterpay, four no-interest installment payments for a long list of products.

In dozens of nations around the world, consumers leverage the power of spaced payment with zero interest via Afterpay’s platform.

Buyers get a fully transparent and no-frills model that is big on convenience and easy on tight budgets. Every few weeks, Afterpay adds more retailers and products to its offerings.

Putting It All Together

The entire concept of shopping and paying online is in a state of change. Retailers, like the ones listed above, are scrambling to give consumers the goods they want along with the simplest and most budget-friendly ways of paying.

Successful online sellers offer people at least one method of delaying payment, while most give potential customers a choice among numerous BNPL arrangements.

Some merchants delay interest for a fixed period or allow for other arrangements that make it simpler to purchase items from every retail category.

Always read the fine print and specific financial conditions before buying from a retailer for the first time. Even though BNPL is usually a good deal, it’s essential to know how much you must pay and when you need to pay it.

Leave a Reply