It’s hard to believe that buying products online was once regarded very warily by a majority of people. In the years since the invention of the web, more and more people have enjoyed the diversity and convenience that online shopping offers them.

Afterpay takes it one step further by offering consumers a way to purchase products without having to pay the full amount upfront.

What Is “Buy Now Pay Later?” Or Shopping on Credit?

Most people are familiar with the concept of layby. This is where you pay for a product bit by bit until it has been completely paid off, at which point you get the product.

The “buy now pay later” option, represented by companies such as Afterpay, reverses this process: you choose the product and pay for it in four fortnightly payments. The great thing is that unlike regular layby, you get to walk out of the store with the product before you’ve even made your first payment!

Better yet, every payment is interest free on Afterpay. This means that there are no hidden costs to inflate the price of the product you want. You pay every two weeks and pay no more than the retail price of the item in question.

However, AfterPay is not the only player in the game. There are several other alternatives which gives consumers multiple options in the market.

In this article we have researched and selected some of the best sites and competitors that are similar to AfterPay and work with the same concept for consumers so let’s see them below (the list below is in no particular order):

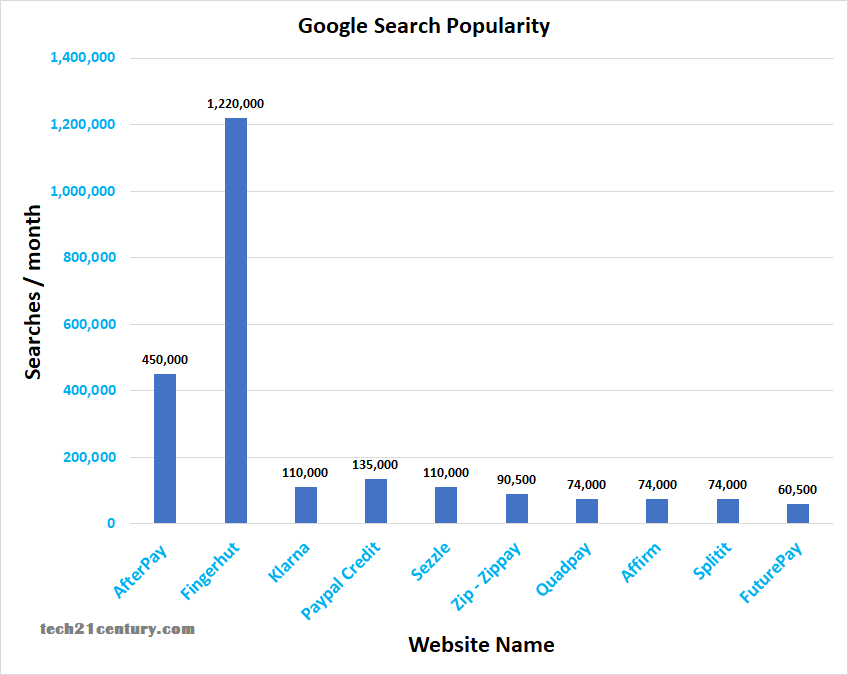

Before getting into our list of sites below, let’s see a chart showing the popularity on Google (based on search queries per month) for some of the websites that we’ll be discussing in the article:

Note that the list below is in no particular order.

1) Klarna

Afterpay is often focused on brick and mortar retailers, but this service also focuses on online commerce. This is what the Stockholm-based Klarna company does.

Shopping with Klarna is as simple as downloading their smartphone application. When you browse their store, you get access to many online retailers who have partnered with Klarna. You get to choose any product, have it shipped to you, and pay for it in four interest-free installments.

If you’re concerned about your privacy, you can create what Klarna calls a Ghost Card. This digital credit card is linked to your real debit or credit card, but acts as a layer between you and the retailer.

You authorize a dollar amount, and then pay with your Ghost Card through the Klarna application. The four payments are deducted and then the Ghost Card expires. You can create one each time you need to shop.

2) Paypal Credit

By leveraging the global power of Paypal, you get access to thousands of products. If you have a Paypal account, you can get access to Paypal credit. For any purchase over $99, you get 6 months to pay the item off in full with no interest added.

3) Sezzle

Sezzle works with a wide variety of online retailers to offer you four easy interest-free payments spread out over six weeks.

This extended time gives many people the ability to ensure that they have the money to pay off the item in full, and may be preferable to some other similar services.

4) Zip

Zip is one of the most well-known buy-now-pay-later operators and works with many retailers. Like Afterpay, it’s not exclusive to online only stores, and many brick and mortar stores support it. And like Afterpay, you get access to an easy-to-use app too.

If you’re approved for a Zip account, you can choose and take home any product you want from a supported store.

Zip then sends a statement of your balance to pay at the start of every month. You can either pay in full or choose to have the payments spread out, interest free, over a set period of time.

5) Quadpay

Quadpay uses the catchy sub title of “any store, split in four” to encapsulate everything they do. Choose any product from a supported store and split the whole payment into four payments over the following six weeks.

This generous time frame allows most people to ensure that they can pay it off and places a lot less pressure on the family budget.

You even get access to a Quadpay Visa digital credit card that you can swipe at any supported retailer. Just use your Quadpay digital card and your purchase will automatically be added to your account and divided into four easy payments.

6) Affirm

Affirm works a bit differently than the above-mentioned services. Whereas companies like Afterpay tend to be most used for small to medium-sized purchases, Affirm allows you to spread out repayments over a much longer period, such as 12 or even 18 months. However, this flexibility does mean that you’ll need to pay interest on those purchases.

When you want to check out at a place like Walmart, for example, all you need to do is choose the Affirm option when checking out with your cart.

You’ll then go through an approval process. If successful, you get the item, but the payments will split up over a number of months with interest. This is a great option if you need to buy something big for your home.

7) Fingerhut

If you don’t have great credit but you really need to build up your credit score or simply need another option for buying products, Fingerhut may be your answer. The good news is that they will consider applicants with poor credit or even no credit.

If you’re approved for Fingerhut credit, you can buy what you like at a supported retailer and they’ll send it out straight away. You then get to split up the total purchase price over time with low monthly payments.

As shown from the popularity chart on top of this article, Fingerhut is the most popular credit service from all.

8) Splitit

Splitit makes it easy to shop with supported retailers. All you need to do is choose the “Pay with Splitit” during the cart checkout process. You can then log into your Splitit account and the product will be added.

The company makes it easy to choose how you want to pay and over how long a time period. You can choose to pay in installments over a fixed period, and can even split the total up to 24 installments.

This flexible payment arrangement is interest-free and allows people to choose an arrangement that suits their budget.

Splitit offers an attractive website and an easy checkout process that offers great flexibility and no interest. In this sense, it offers people an easy way to explore the world of “buy now, pay later” services.

9) Partial.ly

Partial.ly is a great way for businesses to increase their cash flow by offering their customers flexible payment plans. Once a retailer signs up with Partial.ly, they get access to a flexible payment service that allows any of their customers to set up automated payments over time.

While other flexible payment services are aimed at consumers, Partial.ly takes a different approach. It targets businesses who really want to improve their cash flow by offering them flexible payment options.

There are no hidden fees, and even though there are transaction fees that Partial.ly does collect, everything is presented in a transparent and upfront manner.

10) FuturePay

If you primarily shop online, and would like a flexible option for payments over time, FuturePay is a good choice. As the name suggests, you purchase a product and then pay in the future. It could hardly be any easier, and the name really does say it all.

Every charge is transparent with FuturePay and there are no hidden fees or terms. You get to buy your product online and have it sent out.

The balance of the purchase can be paid off with as little as $25 per month until it’s paid in full. If you want to pay it off in full, you can do that too.

If you need another month to make more payments because you just can’t stretch your home budget, you can do that too. For every $50 balance you carry forward into a new month, you are charged a small $1.50 fee.

The great thing about FuturePay is that everything is transparent. The fees are low and the payment terms are flexible. You get the choice of when and how you pay and for how long. This makes it a service worth checking out.

11) Viabill

For those living in the US or Denmark, Viabill is a great alternative.

Viabill similarly allows you to pay for your purchase in 4 installments at an initial limit of $300. But instead of paying after every two weeks, Viabill charges the subsequent installments on the last banking day of each month. This gives you more time to save up and pay for each installment amount.

Viabill similarly charges no interest and hidden fees. Since your registered payment method is automatically charged each month, there are also no penalty fees. How is this possible, you ask? Well, Viabill imposes a fee on its merchants so that they can offer payment by installment.

Thus, shoppers get to enjoy zero interest rates on installment payments with no strings attached. And with over a thousand merchants to choose from, you’ll certainly enjoy shopping with Viabill.

12) Laybuy

Another alternative to Afterpay is Laybuy. This service is available to New Zealand, Australia, and the UK, and offers installment payment for a variety of shops – both for online and in-store transactions.

Unlike After, Laybuy spreads your payment into 6 installment terms which are payable every week. If you fail to pay on time, you will be charged a penalty of $10 or £6.

This tighter payment schedule gives assurance to both the company and the merchants that you are capable of paying.

All things considered, Laybuy is a great choice for those who are running a little short on shopping day but expects to pay the full amount in a short period.

13) Littlewoods

Littlewoods is one of the biggest retail chains in the UK. To make shopping more accessible to its customers, the brand now offers several installment schemes that would cater to the different needs of each shopper.

First, it offers the Spread The Cost Interest-Free program that allows the buyer to make 20-week or 52-week installments at 0% interest. You can pay the installment amount monthly, and this helps you manage your finances better.

The second option is the Buy Now Pay Later program. This allows you to delay payments for up to 12 months at an annual interest that’s calculated upon checkout.

But, if you pay the full amount before the end of your delayed payment schedule, you don’t have to pay the interest. This is the best option if you have to make an emergency purchase when you’re out of cash.

And finally, Littlewoods also offers an interest-free installment option on selected furniture items. You can choose to spread the cost between a 104-week period or a 208-week period.

14) Pay in 4 – Paypal

Paypal is one of the biggest payment platforms around the world, so we weren’t surprised when it announced its own short-term installment service called Pay in 4.

With this service, users get to spread the cost of their purchases in 4 interest-free installments to be paid in six weeks. Qualified customers are given a credit line of around $30 to $600, depending on their capacity to pay. And since Pay in 4 is integrated into your Paypal Wallet, managing your payments won’t be a problem.

But at the moment, Pay in 4 is only available to Paypal users in the US.

15) Atokes

Another alternative to Afterpay is Atokes. This relatively new installment service offers interest-free cost-spreading with varied credit limits.

Qualified members are assessed based on their proof of income and other relevant documents. From there, Atokes assigns a monthly credit limit for each user.

New users are given six months of interest-free installments, which can go up to 10 monthly installments, depending on how well you handle your payments.

To give you a better idea of this service, imagine that you were given a $100/month credit limit and a maximum 6-month installment period. This allows you to buy up to $600-worth of items with the payment spread within 6 months.

But what’s interesting about this Cyprus-based company is that you can also pay an initial amount that can be deducted from the installment amount.

For example, if you want to buy something worth $750 but you’re only allowed to spend $600 for the 6-month period, you can pay an initial amount of $150, so you can stick with the $100/month credit limit.

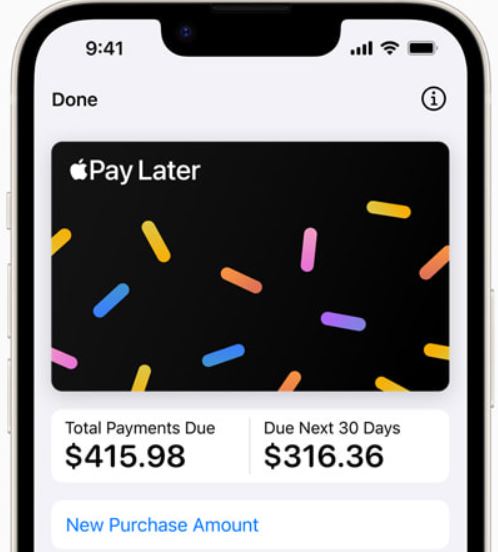

16) Apple Pay Later

The famous Apple Pay Later app has flexible and convenient payment terms that are easily integrated within the larger Apple cyber ecosystem.

The crux of the app is that users can spread their payments over time, even when they choose to make purchases immediately.

All the payout plans are fully transparent and can be highly personalized to match the user’s financial ability and spending habits.

There’s a user-friendly wallet app for real-time payment management, like checking on due dates and logging all transactions.

The app’s high point is security. It employs Apple’s high-tech components to protect transactions and user information. Checkout is easy, fast, and secure, whether you purchase in-store or from online merchants.

17) Uplift

Travelers use Uplift more than any other group because the app is specifically designed for their needs. In addition to booking hotel rooms and flights, users can go on tours and shop while on vacation.

The pay-later aspect is ideal for folks who like the idea of monthly fixed payments and flexible repayment plans that suit their budget and income.

The whole point is to enjoy traveling without worrying about money during a vacation. There’s also trip protection, special low-rate promotional financing terms, travel insurance, and no-interest or very low-interest rates for qualifying users. The app is designed to make traveling affordable and convenient.

18) Four

People using the Four BNPL app get a generous menu of features, like installment payment plans, a vast network of online and traditional retailers integrated with Four, and the signature “four payment” arrangement. The app’s design aims to make it easier for users to manage their budgets.

Those who make their payments on time don’t pay fees or interest. Note that there are fees for missed payments, but the app allows for easy and transparent scheduling. So, tracking your spending and staying on top of payments is simple.

19) Ginny’s

Ginny’s is a leading BNPL app with an extensive menu of worthwhile features. Not only is it generally user-friendly, but you can directly link credit and debit cards to Ginny’s app. That way, partner merchants and service providers offer seamless purchasing for consumers who use Ginny’s BNPL app.

You can pay in installments to make costly items more affordable. In some cases, it’s possible to get zero interest, but that’s only sometimes available.

One unique touch is that Ginny’s app makes individualized recommendations based on your preferences and buying history.

20) Wards

Like Ginny’s, Wards is a prominent provider of BNPL functionality via a proprietary app. However, while Wards offers all the basic fundamentals users expect in today’s BNPL apps, they also throw in a few unique offerings for their users.

With super-secure payment methods and a straightforward signup system, Wards lists many exclusive deals for those using its app.

Additionally, their menu of partner merchants is much more extensive than their competitors. For individuals with varying financial needs, the app has adjustable installment plans and repayment periods longer than usual.

Plus, there are excellent resources for educating users about responsible budgeting and spending, like financial literacy tools.

How does Afterpay work?

Afterpay is an innovative solution that makes shopping more accessible to consumers. It works by providing sellers with an option to offer payment on an installment basis. Particularly, buyers pay the amount in four installments which is billed every two weeks.

Upon sign up, users have to provide payment details which will serve as a security for the payment in case you fail to pay when the installment price becomes due.

While Afterpay allows you to pay by installment at 0% interest, you have to pay a penalty of $10 if you fail to pay on the due date.

Does Afterpay hurt your credit?

There are two things you have to understand the correlation between Afterpay and your credit score.

First, Afterpay merely reserves the right to perform credit checks to verify your capacity to pay. This means that if you’ve been religiously paying your dues on time, this wouldn’t translate to improving your credit history.

However, the same is not the case if you haven’t been able to meet your payment deadlines. Afterpay similarly reserves the right to report negative activity if you failed to pay on time, and that could really hurt your credit score.

Who is eligible for Afterpay?

Afterpay operates in Australia, New Zealand, the USA, and the UK, and each state follows a different set of criteria as to who becomes eligible to avail of the service.

But generally, you have to be at least 18 years old or legally old enough to enter into a contract in your state of residence. You must also be the authorized holder of a credit or debit card.

Other factors that may affect your eligibility include providing a valid email address, phone number, and delivery address in your state of residence.

Does Afterpay have a limit?

Yes. Afterpay promotes responsible spending, which is why it imposes specific maximum spending limits.

Afterpay allows sellers or retailers to set limits per transaction on their shop. This limit is $1,500. The company also set a maximum outstanding limit of $2,000, but this is only made available to users who have already demonstrated a strong repayment behavior.

As to the number of orders, new users are only allowed to make one order in the first 24 hours.

Consequences of Late Payments in Buy Now Pay Later (BNPL)

Consequences of a late payment in a Buy Now, Pay Later (BNPL) plan can include:

- Being charged a late fee.

- The accrual of interest on the unpaid balance.

- Having your account frozen, preventing further transactions.

- Your account being turned over to a collection agency.

- Potential negative impact on your credit score if the BNPL provider reports to credit bureaus.

- Additional bank fees, such as overdraft fees, if payment attempts cause your account to be overdrawn.

Final Words

Sticking to a family budget in the twenty-first century can be tough work. Many people are on restricted budgets and are always looking for a bargain.

Services like Afterpay and others offer just about anyone a flexible payment process that allows them to get the products they need upfront and pay later.

There are a few things to be aware of, however. Some companies do charge interest, so it’s worth calculating whether or not the interest is worth the purchase.

On the other hand, some services are worth using because they offer the ability to make payments over a longer period of time.

It’s also worth noting that these are credit services, so you will need to apply for them. If you don’t pay on time, it can affect your credit score.

Having said that, flexible payment terms are always welcome in an age when unemployment is high and people are often struggling to pay their bills. This provides everyone with a more flexible payment arrangement and is good for both consumers and businesses.

I would like to try this iv heard it’s great

An actual list of bnpl’s around the globe, that took some time to compile:

Addi, Affirm, Afterpay, Alipay, Atokes, Bread, Brighte, Beforepay, Billease, Bundll, Cashalo, Douugh, EmpatKali, Fingerhut, Finzi, Finme, Flipkart, Flexpay, FuturePay, Grab, Gopay, Hoola, Humm, ISentric, Jungle, Klarna, Latitude Pay, Lazy Pay, Laybuy, Open Pay, Partial,ly, Paidy, Paypal, Paytam Postpaid, Credit Payright, Quadpay, Sezzle, Slice, Simpl, Split, Splitit, Tendopay, Uplift, Viabill, Zestmoney, Zebit, Zip.

As you can see, there are too many players offering mirrored services to customers- that means customers are going to rack up different debts on competing bnpl services. It’s going to become like the bad old days of competing credit cards again.

Around 30% of these businesses really shouldn’t exist, imho.